Core Banking Integration

,

Financial Data & Integration

by

Kent Brown

Integrating with the core is hard. In general, the challenges involve legacy systems, data security concerns, regulatory compliance requirements, system complexity, and vendor dependencies. The difficulty is further complicated because each banking core possesses integration nuances specific to its technology. Imagine the impact on innovation in financial services if those subtleties were addressed through standardization. What if connecting your core to a new fintech or application was as easy as plugging in a USB cord on your laptop? This is an oversimplified illustration, but our vision for Open and Reusable Core API (ORCA) is a universal data model that will save our customers the headaches of core integration.

What is Open and Reusable Core API (ORCA)?

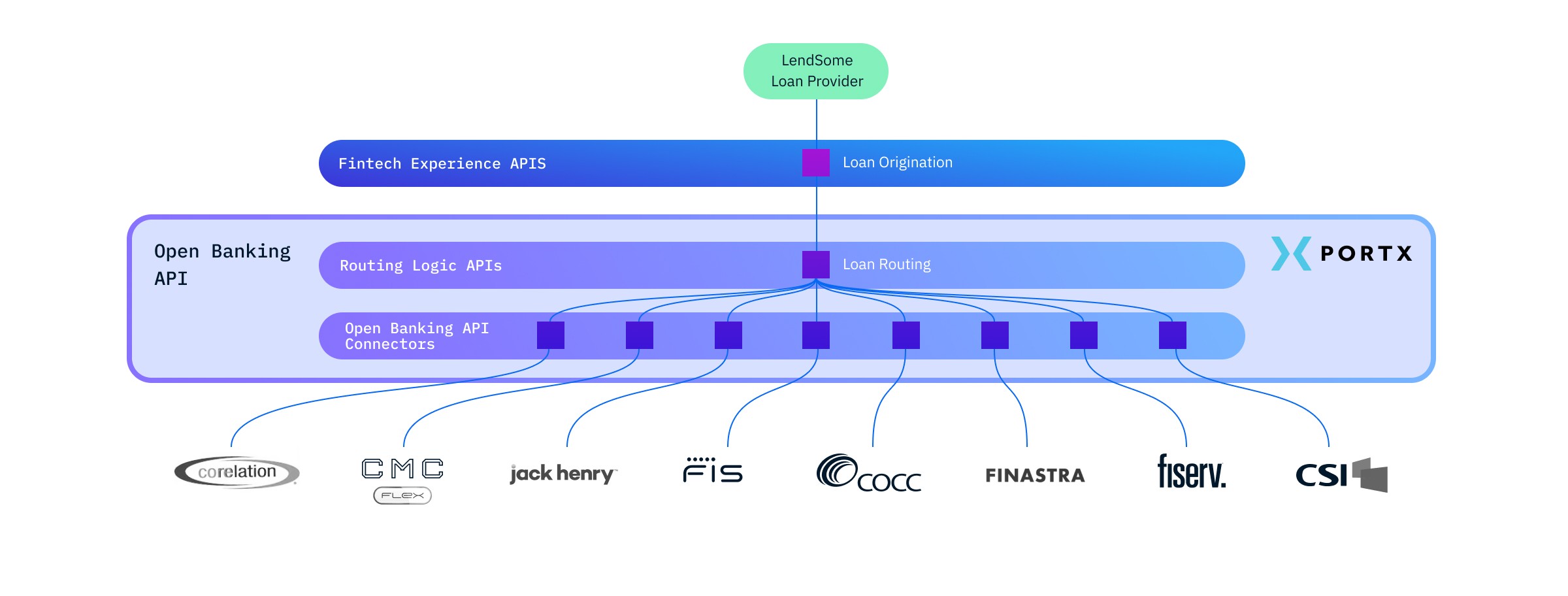

Our team has spent years delivering core integrations for our financial institution (FI) customers. With each project, we collated detailed information required to successfully connect that specific core vendor. Open and Reusable Core APIs (ORCA) will provide a universal API definition that FIs and fintechs can use to implement familiar FI use cases like online banking, digital banking, account opening, loans, etc., and will cover 80-90% of the most common core vendors.

Essentially, ORCA is a set of standardized system APIs (interfaces that expose data from key systems, such as the banking core, in a repeatable manner), delivering a predictable format for common banking operations. This eliminates the need to directly wire business logic to the core. Instead, the FI simply calls the Open Banking API and PortX maps the data to the banking core on the back end, enabling universal connectivity.

How ORCA will unlock flexibility and innovation for FIs

Building ORCA is a substantial endeavor but one we believe will transform how FIs think about their business model and partnerships. ORCA will greatly simplify the mapping and data exchange tasks required for FIs to integrate with cores and, combined with our growing number of core vendor partnerships, will continuously decrease the time it takes to complete that process. Eventually, the solution’s functionality will allow any FI running on an existing ORCA-connected core to “drop in” a pre-built core connector API with only minor adjustments, saving significant development time.

The primary benefit of ORCA is a universal data model that includes pre-built APIs delivering:

REST API interfaces

Common FI use case operations

ISO 20022 standards applied

Our ultimate vision for ORCA is to give FIs the freedom and flexibility to connect any fintech that helps accelerate innovation for their business – including the core vendor. Below, are just a few examples of how ORCA can transform integration and business strategy for FIs:

Quickly onboard new fintechs by allowing the partner to connect with an open banking API instead of the core.

Enable the deployment of multiple use cases over time with only the need to define business and presentation logic for each. Again, no connection to the core is required.

Slowly migrate to a new core while keeping the existing core attached to ORCA. Some of the tasks involved, including data migration and feature gap analysis and adaptation, are outside the scope of ORCA. However, this allows for a phased approach and the old core can be removed at the appropriate time. This enables the addition of multiple cores wired into the same layer, powering the flexibility needed for rapid acquisition of other FIs.

How ORCA will help fintechs scale

In general, fintechs operate on a low-cost model, meaning to scale the number of PortX-connected partners effectively, we had to reduce the time and cost of delivery while ensuring predictability and reliability once the system is up and running. To do so, we implemented a universal and consistent data model with pre-built, tested, and reusable connectors – making ORCA development more affordable and minimizing the cost for fintechs.

To address simplicity, ORCA will provide a single reliable API that fintechs can integrate. That API will be implemented across various cores, creating a kind of “universal adaptor” that enables simplified connectivity with any core on the system. This API mapping provides a significant reduction in work for fintechs as the mapping work is only required once, and ORCA will provide subsequent mapping across all connected cores. In the future, our pre-built, tested, and reliable core connectors will implement this API, minimizing the need for individual API development for each bank – helping fintechs reach new FI customers at scale.

Core integration isn’t as easy as plugging in technology

We have spent years connecting to dozens of core vendors and found there to be one thing they all have in common: it’s extremely challenging. Our goal is not to trivialize the difficulties of connecting to legacy technology but rather to leverage our experiences to smooth out the edges anywhere we can and make the process as pain-free as possible.

Even if connecting to the technology itself can be simplified, there are still the non-technical prohibitive barriers to reckon with. We complement the technical ease of ORCA with helping you to manage the administrative burden of gaining access to the core, including negotiations.

We’re building ORCA to eliminate the need for fintechs and FIs to connect directly to the core and make future integrations faster, easier, and cheaper – saving you from the hard lessons we already learned. Start a conversation with our team or comment below if you want to learn more about our approach.

1.833.667.6789

hello@portx.io